Going public is one of the most expensive transactions a company will ever undertake yet most founders only learn the true price tag after the process is already underway. An Initial Public Offering (IPO) isn't a single fee; it's a stack of overlapping costs that span investment banking, law, accounting, regulatory compliance, and corporate restructuring, and the bill doesn't stop on listing day.

For a company raising $100 million, total IPO costs typically land between $8 million and $12 million in direct expenses, plus several million dollars per year afterward just to remain public. For larger offerings, underwriting fees alone can run into tens of millions, even though the percentage charged tends to shrink as deal size grows.

This guide breaks down every major cost category in an IPO underwriting, legal, accounting, SEC registration, exchange listing, marketing, and advisory fees and compares them against alternatives like direct listings and SPAC mergers. You'll also get a proprietary IPO Cost Readiness Framework, real fee benchmarks from recent filings, and a breakdown of the ongoing costs that continue for years after the opening bell.

By the end, you'll understand not just what an IPO costs, but why the costs are structured the way they are and where founders have realistic room to negotiate.

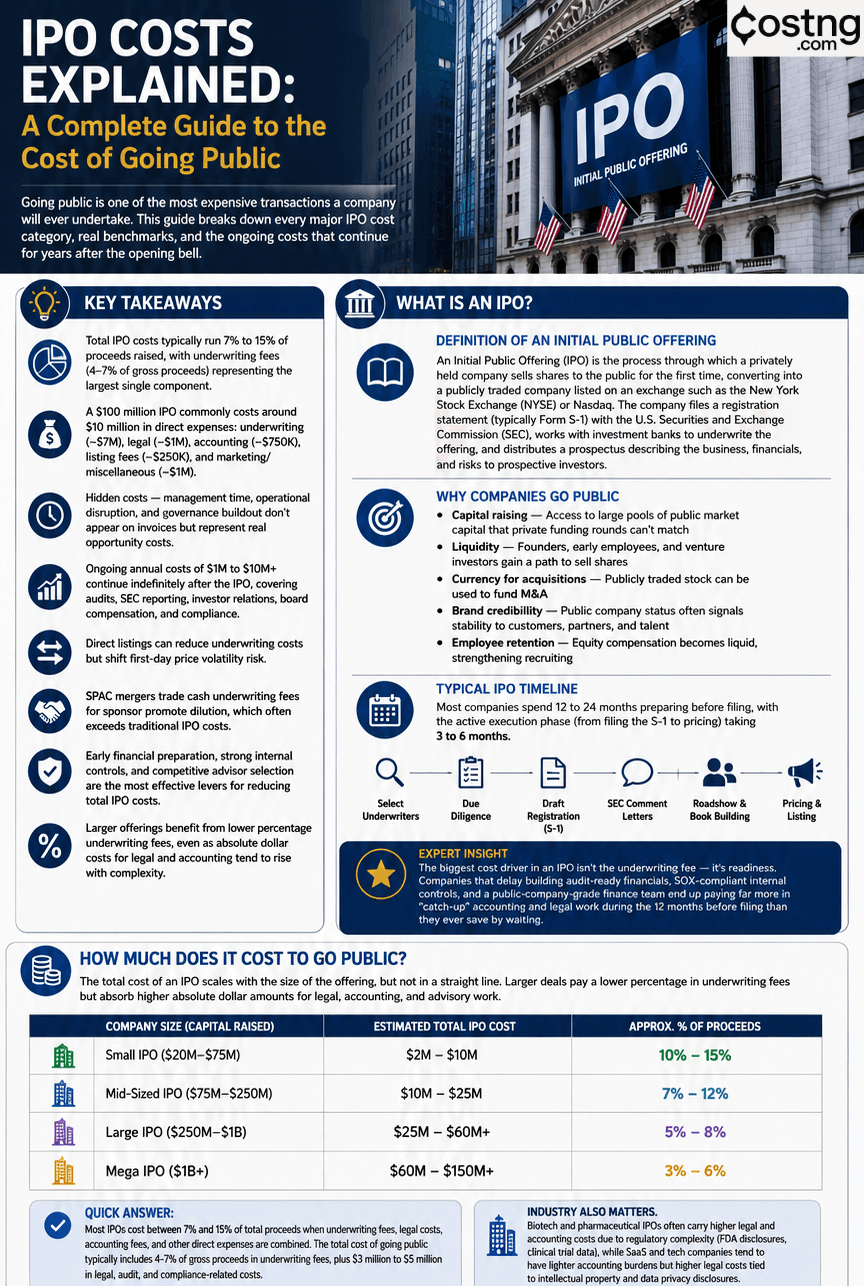

Key Takeaways

- Total IPO costs typically run 7% to 15% of proceeds raised, with underwriting fees (4-7% of gross proceeds) representing the largest single component

- A $100 million IPO commonly costs around $10 million in direct expenses: underwriting (~$7M), legal (~$1M), accounting (~$750K), listing fees (~$250K), and marketing/miscellaneous (~$1M)

- Hidden costs management time, operational disruption, and governance buildout don't appear on invoices but represent real opportunity costs

- Ongoing annual costs of $1M to $10M+ continue indefinitely after the IPO, covering audits, SEC reporting, investor relations, board compensation, and compliance

- Direct listings can reduce underwriting costs but shift first-day price volatility risk

- SPAC mergers trade cash underwriting fees for sponsor promote dilution, which often exceeds traditional IPO costs

- Early financial preparation, strong internal controls, and competitive advisor selection are the most effective levers for reducing total IPO costs

- Larger offerings benefit from lower percentage underwriting fees, even as absolute dollar costs for legal and accounting tend to rise with complexity

What Is an IPO?

Definition of an Initial Public Offering

An Initial Public Offering (IPO) is the process through which a privately held company sells shares to the public for the first time, converting into a publicly traded company listed on an exchange such as the New York Stock Exchange (NYSE) or Nasdaq. The company files a registration statement (typically Form S-1) with the U.S. Securities and Exchange Commission (SEC), works with investment banks to underwrite the offering, and distributes a prospectus describing the business, financials, and risks to prospective investors.

Why Companies Go Public

- Capital raising Access to large pools of public market capital that private funding rounds can't match

- Liquidity Founders, early employees, and venture investors gain a path to sell shares

- Currency for acquisitions Publicly traded stock can be used to fund M&A

- Brand credibility Public company status often signals stability to customers, partners, and talent

- Employee retention Equity compensation becomes liquid, strengthening recruiting

Typical IPO Timeline

Most companies spend 12 to 24 months preparing before filing, with the active execution phase (from filing the S-1 to pricing) taking 3 to 6 months. Key stages include selecting underwriters, conducting due diligence, drafting the registration statement, responding to SEC comment letters, the roadshow and book building process, and final pricing.

Expert Insight: The biggest cost driver in an IPO isn't the underwriting fee it's readiness. Companies that delay building audit-ready financials, SOX-compliant internal controls, and a public-company-grade finance team end up paying far more in "catch-up" accounting and legal work during the 12 months before filing than they ever save by waiting.

How Much Does It Cost to Go Public?

The total cost of an IPO scales with the size of the offering, but not in a straight line. Larger deals pay a lower percentage in underwriting fees but absorb higher absolute dollar amounts for legal, accounting, and advisory work.

| Company Size (Capital Raised) | Estimated Total IPO Cost | Approx. % of Proceeds |

|---|---|---|

| Small IPO ($20M–$75M) | $2M – $10M | 10% – 15% |

| Mid-Sized IPO ($75M–$250M) | $10M – $25M | 7% – 12% |

| Large IPO ($250M–$1B) | $25M – $60M+ | 5% – 8% |

| Mega IPO ($1B+) | $60M – $150M+ | 3% – 6% |

Quick Answer: Most IPOs cost between 7% and 15% of total proceeds when underwriting fees, legal costs, accounting fees, and other direct expenses are combined. The total cost of going public typically includes 4–7% of gross proceeds in underwriting fees, plus $3 million to $5 million in legal, audit, and compliance-related costs.

Industry also matters. Biotech and pharmaceutical IPOs often carry higher legal and accounting costs due to regulatory complexity (FDA disclosures, clinical trial data), while SaaS and tech companies tend to have lighter accounting burdens but higher legal costs tied to intellectual property and data privacy disclosures.

Major IPO Cost Categories

Underwriting Fees

Underwriting fees, also called the gross spread, represent the largest single cost in most IPOs. Investment banks, the lead underwriter (or bookrunner) and the broader syndicate purchase shares from the company at a discount and resell them to investors, pocketing the difference.

Typical Range: Underwriting fees typically fall between 4% and 7% of gross proceeds, depending on offering size and risk profile, with smaller IPOs often quoted at the upper end of that range.

For very large, high-profile offerings, the percentage compresses significantly. The gross spread for an IPO can be higher than 10%, though for a $100 million offering at a 7% spread, the underwriting syndicate would receive $7 million in fees, divided among the underwriters arranging the offering. Historical data through 2025 shows that for IPOs with proceeds between $160 million and $200 million, the vast majority 86.1% had gross spreads of exactly 7.0%, while larger proceed categories saw mean gross spreads drop closer to 6.4% and below.

How the gross spread is split

| Fee Component | Typical Share of Gross Spread | Purpose |

|---|---|---|

| Management Fee | ~20% | Lead underwriter coordination, pricing strategy |

| Underwriting Fee | ~20% | Compensation for underwriting risk |

| Selling Concession | ~60% | Broker-dealer compensation for placing shares |

Key Terms

- Lead underwriter (bookrunner): The investment bank responsible for managing the offering, setting price, and coordinating the syndicate

- Syndicate: The group of investment banks sharing underwriting responsibility and risk

- Incentive fee: An additional discretionary fee, commonly between 0.5% and 1% of gross proceeds, paid on top of the gross spread based on the issuer's satisfaction with IPO performance increasingly common in European and Asian markets

Legal Fees

Securities attorneys draft and review the registration statement (S-1), conduct due diligence, negotiate the underwriting agreement, and manage SEC comment letter responses.

Typical Range: Legal fees during an IPO usually range from $1.5 million to $2 million, though the brief's broader estimate of $500,000 to $5 million+ reflects how much variation exists based on company complexity. Costs can rise significantly if the company has complex corporate structures, international entities, or unresolved compliance matters.

What drives legal costs higher:

- Multiple international subsidiaries requiring cross-border legal review

- Unresolved litigation or IP disputes that must be disclosed

- Complex capital structures (multiple share classes, convertible instruments)

- Industry-specific regulatory disclosures (healthcare, fintech, energy)

Accounting and Audit Fees

Public companies must meet Public Company Accounting Oversight Board (PCAOB) audit standards a significantly higher bar than private company GAAP audits.

Typical Range: Accounting fees typically add $500,000 to $2 million, depending on the company's audit readiness, though companies with multiple years of unaudited financials or complex revenue recognition may see costs climb toward the brief's upper estimate of $3 million+.

This covers:

- Audits of two to three years of historical financial statements under PCAOB standards

- Preparation of pro forma financials for the prospectus

- Comfort letters provided to underwriters

- Remediation of any material weaknesses identified during the audit process

SEC Registration and Filing Fees

The SEC charges a registration fee based on the maximum aggregate offering price, calculated using a rate set by statute and adjusted periodically (typically a small fraction of a percent generally in the range of $100-150 per $1 million registered). While this fee itself is modest compared to underwriting and legal costs, the process of preparing the registration statement drafting the S-1, responding to SEC comment letters, and filing amendments is where the real cost lies, and that work is captured in legal and accounting fees rather than the filing fee itself.

Additional regulatory filings include:

- FINRA filing fee for review of underwriting compensation arrangements

- State "blue sky" registration fees in jurisdictions where shares will be sold (less relevant for exchange-listed national offerings but still applicable in some cases)

Exchange Listing Fees

Both major U.S. exchanges charge an upfront entry fee plus an annual listing fee based on shares outstanding.

Nasdaq (Global Select / Global Market), effective 2026: The entry fee for a company's first listing is $325,000, though companies that submitted applications before January 1, 2026 and listed before February 15, 2026 paid the prior $295,000 rate. Annual All-Inclusive Listing Fees scale with shares outstanding ranging from roughly $59,500 for companies with up to 10 million shares outstanding to $199,000 for companies with over 150 million shares outstanding.

NYSE: NYSE's initial listing fee structure is similarly scaled to shares outstanding, with original listing fees commonly falling in the low hundreds of thousands of dollars and annual fees calculated on a per-share basis subject to minimum and maximum thresholds. Both exchanges also pass through smaller regulatory charges, such as the Consolidated Audit Trail (CAT) fee, which is assessed per executed share transaction.

| Listing Cost | Nasdaq (2026) | NYSE (approximate) |

|---|---|---|

| Entry/Initial Fee | $325,000 | Comparable range, scaled by shares offered |

| Annual Fee (small float) | ~$59,500 | Scaled by shares outstanding, with floor/cap |

| Annual Fee (large float, 150M+ shares) | ~$199,000 | Scaled similarly, capped at upper tier |

A Cost Most Founders Miss: Many companies budget for the entry fee but overlook that annual listing fees increase as a company issues more shares over time through follow-on offerings, equity compensation, or stock splits. A company that lists with 40 million shares outstanding and grows to 160 million within five years will see its annual Nasdaq listing fee more than triple, moving from the lowest tier to the highest.

Marketing and Roadshow Expenses

The roadshow is a multi-city (or virtual) tour where management presents the investment thesis to institutional investors ahead of pricing. Costs include:

- Travel, lodging, and event logistics for management and bankers

- Production of investor presentation materials

- Digital roadshow platforms for virtual investor meetings

- Public relations and media coordination around the listing

Marketing costs typically fall in the $250,000 to $1 million range, though this can vary significantly based on the number of cities visited and whether the roadshow is in-person, virtual, or hybrid. Digital roadshows have meaningfully reduced this line item for many issuers since 2020, as virtual investor meetings replace some though rarely all in-person travel.

Financial Advisory Fees

Beyond the lead underwriters, companies often engage:

- Independent financial advisors to provide a second opinion on valuation and deal structure, separate from the underwriters who have an inherent interest in the outcome

- Valuation specialists for 409A and purchase price allocation work

- Investor relations advisors to build the IR program ahead of and immediately after the listing

These advisory engagements typically range from $200,000 to $1 million depending on scope.

Ongoing Costs After an IPO

Going public isn't a one-time expense. Public companies face recurring annual costs that many founders underestimate.

Estimated Annual Range: $1M – $10M+, scaling with company size and complexity.

Annual Audit Costs

Annual PCAOB audits, quarterly reviews, and SOX 404 internal control attestations are recurring requirements. Companies that were "accelerated filers" or "large accelerated filers" face the additional cost of auditor attestation over internal controls, which can add hundreds of thousands of dollars annually compared to a private company audit.

SEC Reporting Requirements

Public companies must file:

- Form 10-K (annual report)

- Form 10-Q (quarterly reports, three times per year)

- Form 8-K (current reports for material events)

- Proxy statements (DEF 14A) for annual shareholder meetings

Each filing requires legal review, financial preparation, and often outside counsel involvement a recurring cost that didn't exist as a private company.

Investor Relations Programs

A functioning IR program includes:

- Dedicated IR staff or outside IR firm

- Earnings call production and transcription services

- Analyst relationship management

- Annual report design and shareholder communications

Board Compensation

Independent directors at public companies typically receive both cash retainers and equity grants a cost that scales with company size but commonly runs into the hundreds of thousands of dollars annually per director when board fees, committee fees, and equity are combined across a full board.

Compliance Programs

Ongoing SOX compliance, internal audit functions, and corporate governance monitoring require dedicated staff often a controller, internal audit team, and compliance officer roles that many private companies don't need.

| Ongoing Cost Category | Annual Estimate |

|---|---|

| Audit & SOX 404 attestation | $300K – $2M+ |

| SEC reporting & legal | $250K – $1.5M |

| Investor relations | $200K – $1M |

| Board compensation | $500K – $3M (full board) |

| Compliance/internal audit staff | $300K – $2M |

| Total | $1.5M – $10M+ |

IPO Cost Example: Company Raises $100 Million

| Cost Category | Estimated Cost |

|---|---|

| Underwriting | $7M |

| Legal | $1M |

| Accounting | $750K |

| Listing Fees | $250K |

| Marketing | $500K |

| Miscellaneous | $500K |

| Total | ~$10M (≈10% of proceeds) |

This example reflects a fairly typical mid-sized U.S. IPO. Note that the underwriting fee dominates the total roughly 70% of all direct costs which is why negotiating the gross spread, even by half a percentage point, has an outsized impact on net proceeds.

IPO Costs by Company Size

Startup IPO (Sub-$75M Raise)

Smaller companies face the steepest cost-to-proceeds ratio. Fixed costs legal minimums, audit fees, exchange entry fees don't scale down proportionally with deal size, so they consume a larger percentage of smaller raises. Smaller IPOs are typically quoted at the upper end of the underwriting fee range, especially when the deal requires more market education or book-building effort.

Mid-Market IPO ($75M–$250M)

This is the range where most "typical" IPO cost benchmarks apply roughly 7–12% of proceeds in total direct costs, with underwriting fees commonly in the 5–7% range.

Enterprise IPO ($250M+)

Larger proceeds categories see meaningfully lower mean gross spreads, and extremely large offerings can achieve gross spreads as low as 1.2%, as was the case with Alibaba's IPO which still amounted to $261 million in fees due to the sheer scale of the offering. At this scale, legal, accounting, and advisory costs become a much smaller percentage of total proceeds, even as their absolute dollar values increase due to deal complexity.

Revenue Thresholds and Complexity: As a general rule, companies generating under $50 million in annual revenue face the highest relative IPO costs and the most scrutiny from underwriters regarding growth trajectory. Companies above $200 million in revenue typically have more negotiating leverage on underwriting fees and access to a wider pool of competing banks.

IPO vs. Direct Listing Cost Comparison

A direct listing allows a company to list shares on an exchange without a traditional underwritten offering existing shareholders sell directly to the public, and no new shares are necessarily issued.

| Cost Area | Traditional IPO | Direct Listing |

|---|---|---|

| Underwriting | High (4–7% gross spread) | Lower banks act as financial advisors, not underwriters, often for flat fees |

| Marketing/Roadshow | High | Moderate investor day replaces traditional roadshow |

| Legal & Accounting | Similar | Similar (same SEC registration requirements apply) |

| Regulatory (SEC) | Similar | Similar |

| Capital Raised | Company raises new capital | Traditionally no new capital raised (though hybrid direct listings now allow this) |

| Lock-up Periods | Standard 180-day lock-up | Often shorter or absent |

Direct Listing Trade-off: While direct listings reduce underwriting costs, they shift risk in a way that isn't captured in a simple fee comparison. Without underwriters committing to purchase and stabilize shares, direct listings can experience more price volatility on the first trading day. For companies prioritizing cost savings over price stability, this trade-off matters and it's a major reason direct listings have remained more common among companies with strong existing brand recognition (where extensive marketing isn't needed to build investor demand).

IPO vs. SPAC Cost Comparison

A SPAC (Special Purpose Acquisition Company) merger allows a private company to become public by merging with an already-listed shell company.

Key cost differences:

- Dilution: SPAC sponsors typically retain a "promote" commonly around 20% of the SPAC's shares which dilutes the value received by the operating company's shareholders. This is a cost not present in a traditional IPO.

- Sponsor shares: The sponsor's founder shares represent a transfer of value that effectively functions as a fee, even though it isn't paid in cash.

- Advisory fees: SPAC mergers (de-SPAC transactions) still involve significant legal, accounting, and advisory fees comparable to a traditional IPO, since the combined company must still meet SEC reporting and exchange listing requirements.

- Transaction costs: PIPE (private investment in public equity) financing is often needed alongside the SPAC merger to ensure sufficient cash remains in the combined company, and PIPE placement agents charge their own fees.

Bottom line: SPAC mergers can offer a faster path to public markets and more price certainty (since valuation is negotiated rather than discovered through a roadshow), but the dilution from sponsor promote shares often exceeds what a company would pay in underwriting fees through a traditional IPO a trade-off that became widely scrutinized following the SPAC boom of 2020–2021.

Ways to Reduce IPO Costs

Early Financial Preparation

The single highest-leverage action a company can take is building audit-ready, GAAP-compliant financials 18–24 months before an intended IPO date. Companies that wait until the IPO process begins to clean up their books pay significantly more in accounting fees for "catch-up" audits and remediation work.

Strong Internal Controls

Investing in SOX-ready internal controls before the IPO process begins reduces both audit fees (auditors spend less time testing weak controls) and legal risk (fewer disclosed material weaknesses in the prospectus).

Selecting the Right Advisors

Running a competitive process among underwriters rather than defaulting to a single relationship bank creates leverage to negotiate the gross spread. Similarly, engaging legal counsel with deep IPO experience in your specific industry reduces billable hours spent on learning curve issues.

Efficient Due Diligence

A well-organized data room with complete, indexed documentation reduces the hours legal and accounting teams spend searching for information directly lowering professional service fees, which are typically billed hourly or against a capped fee arrangement that assumes a reasonable level of organization.

The IPO Cost Readiness Framework

To help founders self-assess before engaging bankers, here's a practical framework for evaluating IPO cost exposure across five dimensions:

| Readiness Dimension | Low Cost Risk | High Cost Risk |

|---|---|---|

| Financial Audit History | 2-3 years of clean PCAOB-ready audits already completed | Financials require restatement or first-time PCAOB audit |

| Corporate Structure | Single entity or simple holding structure | Multiple subsidiaries, international entities, complex cap table |

| Internal Controls | Documented SOX-ready controls in place | Informal processes requiring full buildout |

| Industry Complexity | Standard disclosure requirements (e.g., SaaS) | Heavy regulatory disclosure (biotech, fintech, energy) |

| Governance Structure | Independent board members already recruited | Board requires significant restructuring pre-IPO |

A company scoring "high cost risk" across most dimensions should expect to spend toward the upper end of every range in this guide and should budget an additional 12-18 months of preparation time to move toward "low cost risk" before initiating the formal IPO process, which can meaningfully reduce both legal and accounting fees during execution.

Is Going Public Worth the Cost?

For many companies, yes, but the decision depends on weighing the costs above against the strategic benefits:

Benefits:

- Access to capital: Public markets provide access to far larger pools of capital than most private funding rounds, and ongoing access through follow-on offerings

- Liquidity benefits: Founders, employees, and early investors gain a path to realize value from their equity

- Brand credibility: Public company status can improve standing with enterprise customers, suppliers, and talent

- Acquisition currency: Publicly traded stock becomes usable for M&A

Costs and trade-offs:

- Increased regulatory burden: Ongoing SEC reporting, SOX compliance, and governance requirements represent a permanent increase in operating costs

- Loss of confidentiality: Competitors gain visibility into financial performance

- Market pressure: Quarterly reporting can create pressure toward short-term decision-making

The right answer depends heavily on company size, growth trajectory, and capital needs. Companies that can access sufficient capital through late-stage private rounds and don't have urgent liquidity needs for early investors may reasonably delay an IPO to avoid the ongoing cost burden, while companies needing significant capital for expansion or facing investor pressure for liquidity events often find the costs justified.

Frequently Asked Questions

How much does an IPO cost?

Total IPO costs typically range from $2 million for small offerings to $50 million or more for large offerings, generally representing 7% to 15% of total proceeds raised. The largest component is underwriting fees, commonly 4-7% of gross proceeds.

What is the largest IPO expense?

Underwriting fees (the gross spread) are almost always the largest single expense, typically representing 60-70% of total direct IPO costs.

What percentage do underwriters charge?

Underwriting fees typically fall between 4% and 7% of gross proceeds, with smaller offerings at the higher end and very large offerings sometimes falling below 4%, occasionally as low as 1-2% for mega-deals.

Are IPO costs tax deductible?

IPO-related costs receive mixed tax treatment. Generally, costs directly related to the issuance of stock (such as underwriting fees and certain legal costs tied to the offering itself) are treated as a reduction of the proceeds raised rather than as a deductible business expense, while other costs may be deductible as ordinary business expenses. This is a complex area where companies should consult a tax professional, as treatment can vary based on the specific nature of each cost.

How much does it cost to stay public?

Ongoing annual costs for being a public company typically range from $1 million to $10 million or more, covering annual audits, SEC reporting, investor relations, board compensation, and compliance programs.

Is a direct listing cheaper than an IPO?

Direct listings generally reduce underwriting-related costs since no traditional underwriting syndicate is purchasing and reselling shares, but legal, accounting, and SEC registration costs remain similar. The overall savings depend on the specific deal structure.

How long does the IPO process take?

Most companies spend 12-24 months preparing before filing, with the active execution phase from initial filing to pricing taking approximately 3-6 months.

Can small businesses afford an IPO?

Small companies face the highest cost-to-proceeds ratio because many IPO costs (legal minimums, audit fees, exchange entry fees) don't scale down proportionally with deal size. This is why companies below a certain revenue threshold often pursue alternative funding sources, such as continued private equity or venture capital, before considering an IPO.

How much does Nasdaq charge to list a company?

As of 2026, Nasdaq's entry fee for a company's first listing on the Global Market or Global Select Market is $325,000, and annual All-Inclusive Listing Fees range from approximately $59,500 to $199,000 depending on total shares outstanding.

How much does NYSE charge to list a company?

NYSE charges an initial listing fee in a comparable range to Nasdaq's entry fee, plus annual fees calculated based on shares outstanding subject to minimum and maximum thresholds. Exact fees vary by company size and should be confirmed directly with NYSE's current price schedule.